Debt Management: Your Step-by-Step Plan to Debt Freedom in 3-5 Years

Debt management strategies offer a structured approach to eliminate debt within 3–5 years by creating a detailed financial plan. This involves assessing debts, budgeting, and utilizing methods such as debt consolidation or the debt snowball to achieve financial stability and freedom.

Feeling overwhelmed by debt? You’re not alone. Many Americans struggle with managing their finances and finding a way out of debt. The good news is that effective debt management strategies can help you create a step-by-step financial plan to eliminate your debt within 3-5 years, bringing you closer to financial freedom.

Understanding Your Debt Landscape

Before diving into debt management strategies, it’s crucial to understand the specifics of your current financial situation. This involves taking a close look at your outstanding debts, their interest rates, and the minimum payments required. This comprehensive overview will lay the groundwork for a successful debt elimination plan.

Assess Your Debts

The first step is to list all your debts, including credit cards, student loans, auto loans, and personal loans. For each debt, note the outstanding balance, interest rate, and minimum monthly payment. This detailed assessment will provide a clear picture of where your money is going each month.

Calculate Your Debt-to-Income Ratio (DTI)

Your DTI is the percentage of your gross monthly income that goes toward paying your debts. To calculate it, divide your total monthly debt payments by your gross monthly income. A high DTI indicates that a significant portion of your income is allocated to debt, which may require more aggressive debt management strategies.

- List all debts: Include balances, interest rates, and minimum payments.

- Calculate DTI: Divide total debt payments by gross monthly income.

- Identify high-interest debts: Prioritize these for faster repayment.

Understanding your debt landscape helps tailor your approach. By identifying high-interest debts and calculating your DTI, you can prioritize your repayment efforts effectively. Knowledge is power when managing debt.

Creating a Realistic Budget

A budget is the foundation of any successful financial plan. It helps you track your income and expenses, identify areas where you can cut back, and allocate more funds toward debt repayment. A realistic budget is not about deprivation; it’s about making informed choices to achieve your financial goals.

Track Your Income and Expenses

Start by tracking all your income sources, including your salary, freelance work, and investments. Then, track your expenses for at least a month to understand where your money is going. Use budgeting apps, spreadsheets, or pen and paper to record your spending.

Identify Areas to Cut Back

Once you’ve tracked your expenses, analyze your spending habits to identify areas where you can reduce costs. Common areas include dining out, entertainment, and non-essential subscriptions. Even small cuts can add up over time and free up funds for debt repayment.

Creating a budget involves honest self-assessment. Are you overspending on certain categories? Can you find cheaper alternatives for some of your expenses? These insights are vital for reshaping your financial habits.

- Track income and expenses: Use apps or spreadsheets to monitor your cash flow.

- Identify spending leaks: Cut back on non-essential expenses.

- Set realistic goals: Aim for sustainable changes, not drastic measures.

A well-structured budget is not merely a list of numbers; it’s a reflection of your financial priorities. By tracking your income and expenses and making conscious spending choices, you can create a budget that supports your debt management goals.

Choosing the Right Debt Repayment Strategy

Selecting the right debt repayment strategy is essential for accelerating your debt elimination process. Two popular methods are the debt snowball and the debt avalanche. Each has its advantages, and the best choice depends on your financial situation and personal preferences.

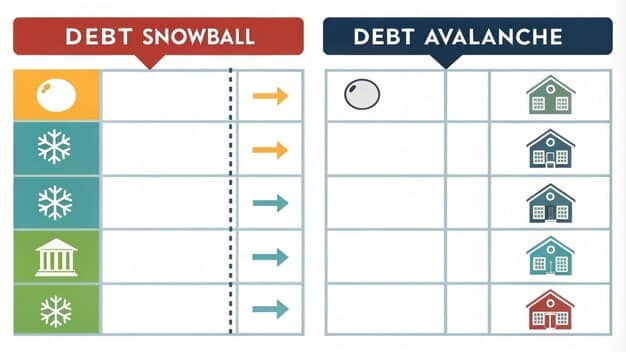

Debt Snowball Method

The debt snowball method involves paying off your debts in order of smallest balance to largest, regardless of interest rate. The idea is to gain quick wins by eliminating smaller debts, which can provide motivation and momentum to tackle larger debts. This method is psychologically rewarding.

Debt Avalanche Method

The debt avalanche method focuses on paying off debts in order of highest interest rate to lowest. This approach saves you the most money in the long run since you’re reducing the amount you pay in interest. However, it may take longer to see initial results.

The choice between the debt snowball and avalanche methods depends on your priorities. Do you value quick wins and psychological boosts, or are you more focused on minimizing long-term interest costs?

- Debt Snowball: Pay off smallest debts first.

- Debt Avalanche: Prioritize high-interest debts.

- Consider your preferences: Choose a method that motivates you.

Selecting the right debt repayment strategy is a personal decision. By understanding the pros and cons of each method, you can choose the approach that best aligns with your financial goals and behavioral tendencies, maximizing your chances of success.

The Power of Debt Consolidation

Debt consolidation involves combining multiple debts into a single new loan, often with a lower interest rate. This can simplify your repayment process and potentially save you money. However, it’s essential to carefully evaluate the terms and conditions of any debt consolidation offer.

Benefits of Debt Consolidation

One of the primary benefits of debt consolidation is simplification. Instead of managing multiple debts with varying due dates and interest rates, you only have one monthly payment to worry about. Additionally, if you can secure a lower interest rate, you may save money over the life of the loan.

Potential Drawbacks

While debt consolidation can be beneficial, it’s not without its risks. Some debt consolidation loans come with high fees or unfavorable terms. It’s crucial to compare offers carefully and ensure that the new loan truly benefits you. Also, be wary of extending the repayment term, as this could result in paying more in interest over time.

Debt consolidation can be a powerful tool, but it requires due diligence. Evaluate all aspects, including fees, interest rates, and repayment terms. Only proceed if the new loan offers genuine advantages over your current situation.

- Simplify repayments: Consolidate multiple debts into one.

- Lower interest rates: Seek favorable terms to save money.

- Evaluate carefully: Watch out for high fees and extended repayment terms.

Debt consolidation can be a valuable strategy for streamlining your finances, but it requires a thorough understanding of the terms and conditions involved. By carefully evaluating your options, you can determine whether debt consolidation is the right choice for you.

Negotiating with Creditors

Don’t underestimate the power of negotiation. Creditors may be willing to work with you to create a more manageable repayment plan. Contacting them and explaining your situation can sometimes lead to lower interest rates or more flexible payment terms. It doesn’t hurt to ask.

How to Approach Creditors

When contacting creditors, be polite, honest, and proactive. Explain your financial situation and why you’re having difficulty making payments. Ask if they can offer any assistance, such as a lower interest rate, a temporary payment reduction, or a modified repayment plan.

Document Everything

Keep a record of all your communication with creditors, including the dates, times, and names of the representatives you spoke with. Save any written agreements or correspondence. This documentation can be helpful if any disputes arise in the future.

Negotiating with creditors requires a proactive and transparent approach. Be honest about your situation and clearly communicate your needs. With persistence, you may be able to secure more favorable repayment terms.

- Be proactive: Contact creditors to discuss options.

- Request assistance: Ask for lower rates or flexible terms.

- Document communication: Keep records of all interactions.

Negotiating with creditors is a valuable skill in debt management. Remember, creditors are often willing to work with borrowers rather than risk non-payment. By being proactive and communicative, you can improve your chances of securing more manageable repayment terms.

Avoiding Future Debt

Once you’ve successfully eliminated your debt, it’s crucial to take steps to avoid accumulating debt again in the future. This involves making long-term behavioral changes and adopting responsible financial habits. Prevention is always better than cure.

Build an Emergency Fund

An emergency fund can help you cover unexpected expenses without resorting to credit cards or loans. Aim to save at least 3-6 months’ worth of living expenses in a liquid, easily accessible account. This will provide a financial cushion during tough times.

Live Below Your Means

Living below your means involves spending less than you earn. This allows you to save money, invest for the future, and avoid relying on debt to finance your lifestyle. Be mindful of your spending habits and make conscious choices about where your money goes.

Avoiding future debt requires a fundamental shift in mindset. Embracing frugality, building an emergency fund, and living below your means are key strategies for maintaining long-term financial stability.

- Build an emergency fund: Save 3-6 months of living expenses.

- Live below your means: Spend less than you earn.

- Stay disciplined: Avoid impulsive spending and unnecessary debt.

Preventing future debt is as important as eliminating current debt. By adopting responsible financial habits and making conscious choices about your spending, you can achieve lasting financial security and avoid the pitfalls of debt accumulation.

| Key Point | Brief Description |

|---|---|

| 📊 Assess Debts | List debts, rates, & minimum payments for clarity. |

| 📝 Create Budget | Track income/expenses, identify areas for cuts. |

| 💸 Debt Strategy | Choose snowball (small) or avalanche (high-interest). |

| 🤝 Negotiate | Contact creditors for lower rates and better terms. |

Frequently Asked Questions

▼

Debt management involves strategies to efficiently pay off debts. It’s important as it reduces stress, saves money on interest, and improves financial stability.

▼

Start by tracking your income and expenses. Identify areas where you can cut back, and allocate more funds towards debt repayment. Use budgeting apps or spreadsheets.

▼

The debt snowball method involves paying off debts from smallest to largest balance. This allows you to see quick wins, providing motivation to continue.

▼

Debt consolidation combines multiple debts into a single loan, often with a lower interest rate. This simplifies payments and potentially saves money.

▼

To avoid future debt, build an emergency fund, live below your means, and avoid impulsive spending. Disciplined financial habits are key.

Conclusion

Implementing these debt management strategies requires commitment and discipline, but the rewards are well worth the effort. By creating a detailed financial plan and sticking to it, you can eliminate your debt within 3-5 years and enjoy the peace of mind that comes with financial freedom. Start today and take control of your financial future.